Instead of Cutting Expenses, Consider Growing Out of Your Expenses

To Investors

Last week I had a conversation with a friend of mine who is a high level operator in the logistics space. She mentioned how one operating region for her global company is going through a rough period where that region has ~$1 million in annual expenditures as a hurdle figure, before accounting for salaries and operational expenses, and that this was unusual when comparing with other regions of her business.

I asked her what the fix was for that situation?

Her response was that there is no fix, and that they have to grow out of it.

That got me thinking about Uber and how as of their financial year ended 2023 there was a lot of excitement that Uber is now profitable for the first time since the company went public, to the point where Uber is planning a $7 billion share buyback program.

I was keen to see how Uber became profitable, and in my research I realised that they really did grow out of their high expenditure problems.

This first chart shows Uber’s revenue and expenditure growth, both showing a positive trend. Normally people would say “cut expenditures” but Uber leaned more towards “grow revenue”.

But perhaps this next chart illustrates the point of growing out of expenses more.

Here we see that since 2020 revenue for Uber has really taken off, printing a 49% rate of annual compound growth while Uber had operating losses.

Remember we had that thing called lockdowns in 2020 when the Covid-19 pandemic spread globally? Since then we all started to prefer delivery rather than going out to stores to shop for groceries or go to restaurants to buy food.

Noting the significance of research and development expenditure by Uber from the first chart, this next chart shows Uber’s revenue by segment.

To highlight, from 2017 to 2023 Uber’s mobility revenue (ride hailing business) only grew at an annual compound rate of 18%, and their delivery revenue (mainly UberEats) grew at a 66% compound annual growth rate.

It's important to note that had Uber not been investing heavily in their delivery business, when the pandemic hit the company may not have seen the amount of revenue growth they’ve seen, especially since 2020.

From 2024 onwards revenue for Uber will continue to grow as they add the London black cabs on their platform, and in New York as they add the ability to hail the infamous yellow cabs. In China Uber still has an investment in Didi, China’s most popular ride hailing service, however I see a path where Uber enters every country in the world to offer a platform approach for each country’s transportation industry without competing too much with existing ride hailing/transportation services.

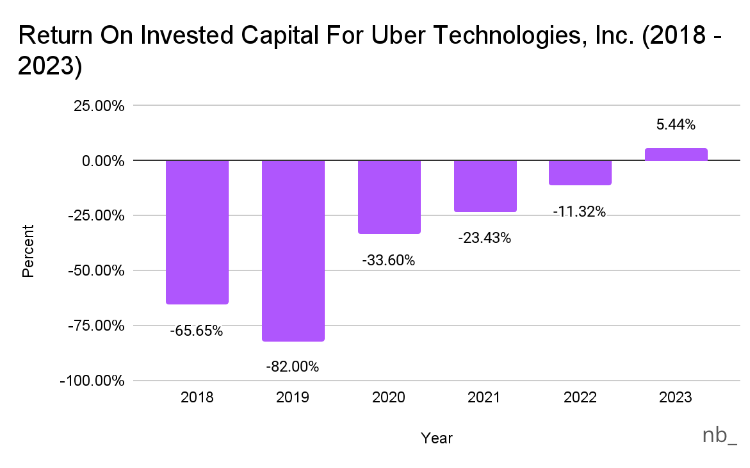

I also couldn't help but look at the return on invested capital (ROIC) for Uber to see the company’s efficiency in generating returns from its capital investments. I think that a crucial part of growing out of expenses is allocating expenditure effectively to allow your revenue to bloom. In the chart below we see steady improvement in ROIC and validation that Uber’s executives are efficient capital allocators, with Uber’s ROIC going from -66% in 2018, to ~5% in 2023.

I would be remiss to also not look at Uber’s cash balance - a vital key performance indicator for any company - noting Uber’s planned $7 billion share buyback program announced earlier this year.

Uber was burning cash from 2017 to 2021, however there appears to be a positive trend on Uber’s free cash flow from 2017 to 2023, where the company now has a free cash flow balance of $3.3 billion.

A loss-making company (and a cash-poor one) would never buy back shares.

Uber announcing a share buyback program signals belief by Uber executives that Uber has finally found its stride operationally and is now making a transition from growth-only, to growth plus maturity, as the company looks to cement its place as the number one global platform for transportation.

The market seems to share the same sentiment; year-to-date Uber is up 17% vs +12% for the S&P 500, and -29% for Lyft.

Next time when people suggest that your company cuts expenses, maybe also consider growing out of your expenses.

I hope you enjoyed reading this letter.

On the journey to becoming a master capital allocator, one lesson down, a billion more to go.

We’ll talk again soon,

-Mansa

If you liked this post, feel free to hit the subscribe button and share with someone who might also find this interesting.

Disclaimer: this note is not financial advice and is for informational purposes only. We may hold positions in the companies discussed. Do your own research