How Much of Your Company Do You Really Own?

How Much of Your Company Do You Really Own?

The Cap Table

To Investors,

Not long ago I saw a concerning cap table, where at the seed stage investment round, the founder of a startup owned only about 13% of his company. The next largest shareholder was at 7%, and there was a lengthy list of other smaller shareholders, plus upcoming convertible debt that was due to mature soon.

A few reasons may have led to a scenario like this: 1) The founder needed to raise a ton of money early on because of the nature of the business; 2) the founder did not adequately forecast the business’s capital needs; 3) the founder did not explore sufficient support systems and funding options such as joining an accelerator, or relevant grant funding; 4) the company’s burn rate was mismanaged; or 5) the company’s cap table was mismanaged.

Whatever the reason, the cap table was mismanaged.

Today, we'll demystify the cap table, touch on two common funding mechanisms for startups (convertible debt and SAFEs), and highlight key considerations for both founders and investors.

What is a Cap Table?

A capitalisation table (or cap table) is a ledger that outlines the ownership structure of a company. It lists all stakeholders, including founders, investors, employees who own shares, and any other parties who hold equity or options in the company. The cap table provides a snapshot of who owns what percentage of the company, which is crucial for decision-making, fundraising, and understanding the potential dilution effects of future investment rounds.

Let's run through a quick example…

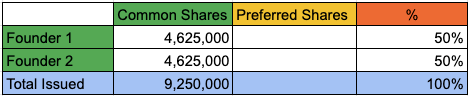

TechCo has 2 founders who each have 50% ownership in TechCo, where 9 250 000 common shares were issued.

At some point the founders will decide to raise funds to hire more people or invest in value enhancing tools for TechCo.

Among the funding instruments that startups use to raise money, convertible debt and SAFE notes appear to be quite common.

Convertible Debt

Allows startups to raise capital through loans that can convert into equity at a later stage, usually during a future financing round.

Debt has an interest rate and a maturity date. Once that maturity date falls due, the debt can legally be automatically converted into equity, diluting existing shareholders.

Simple Agreement for Future Equity (SAFE)

Introduced by Y Combinator, SAFEs are contractual agreements that entitle investors to future equity upon the occurrence of specified triggering events, such as a subsequent priced equity financing round.

TechCo then chooses to raise $1 million in SAFEs to hire more staff from 2 investors; A and B, each with terms as follows:

Investor A: offers $200 000 at a $4 million post money valuation.

Investor A would then have 5% ($200k/$4M) of the company.

Investor B: offers $800 000 at an $8 million post money valuation.

Investor B would then own 10% ($800k/$8M) of the company.

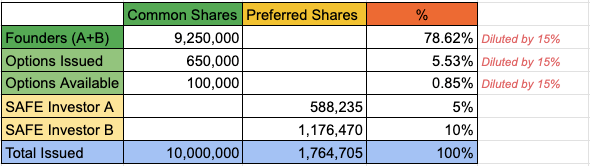

*** Dilution = 5% + 10% = 15%. ***

Because the SAFE does not yet represent shares in the company, the cap table remains as it is in the illustration above, however the founders should always keep in mind that their ownership is now diluted by 15% - which is the amount of equity they sold to Investors A and B.

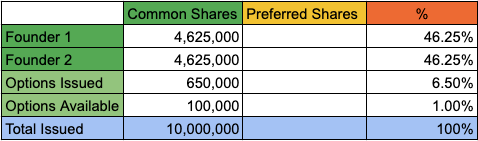

After the $1million raise, TechCo allocates shares (i.e. Options) to be issued to the new early hires. In this scenario the cap table now looks as follows, where 750 000 shares are allocated to the employee option pool, or 7.5% of the company.

6 months later TechCo consults an experienced investor to lead a $5 million Series A investment round at a post money valuation of $20 million.

This is now a triggering event which repopulates the cap table to consider the SAFEs issued to Investors A and B.

Before the incoming $5 million is allocated equity in TechCo, the cap table is immediately recalculated to look as follows:

This is now the base from which the share allocations will be calculated for this new $5 million raise.

For more context and understanding I’ll link a video explainer about SAFEs and dilution at the end.

Things to Look Out For

For Founders:

Dilution: Be mindful of the dilution effects of each fundraising round on existing shareholders' ownership percentages.

Valuation: Striking the right balance between attracting investment and maintaining a fair valuation is crucial to avoid over-dilution.

Investor Relations: Cultivate transparent communication with investors and ensure alignment of interests to foster long-term partnerships.

Be Protective: Shares in your startup must only be given to those that truly provide value. Unless your best friend, or a family member contributes significantly to your startup; do not give them equity. You’ll need that equity one day!

For Investors:

Terms and Conditions: Scrutinise the terms of convertible debt or SAFEs, including conversion triggers, valuation caps, and discount rates, to assess the potential returns and risks.

Founder-Investor Alignment: Evaluate the founder's vision, commitment, and ability to execute the business plan to gauge the likelihood of success and alignment with your investment goals.

Exit Strategy: Understand the company's potential exit opportunities, such as acquisition or IPO, and assess the likelihood of achieving substantial returns on your investment.

As much as the cap table can get a little tricky, as a founder you need to have your house in order, and cap table management is paramount to the success of your business; protecting you, exiting investors, your team, your employees, the company, and the company’s ability to raise additional funding to continue doing great work - especially in those early years.

Luckily there are great cap table management platforms such as Carta and AngelList, otherwise just keep it simple and maintain an updated Excel spreadsheet of ownership in the company.

Always consult a professional investor and keep building!

Respectfully,

-Mansa

For more context here’s a great video explainer on SAFEs

Disclaimer: this note is not financial advice and is for informational and entertainment purposes only. We may hold positions in the companies discussed. Do your own research.